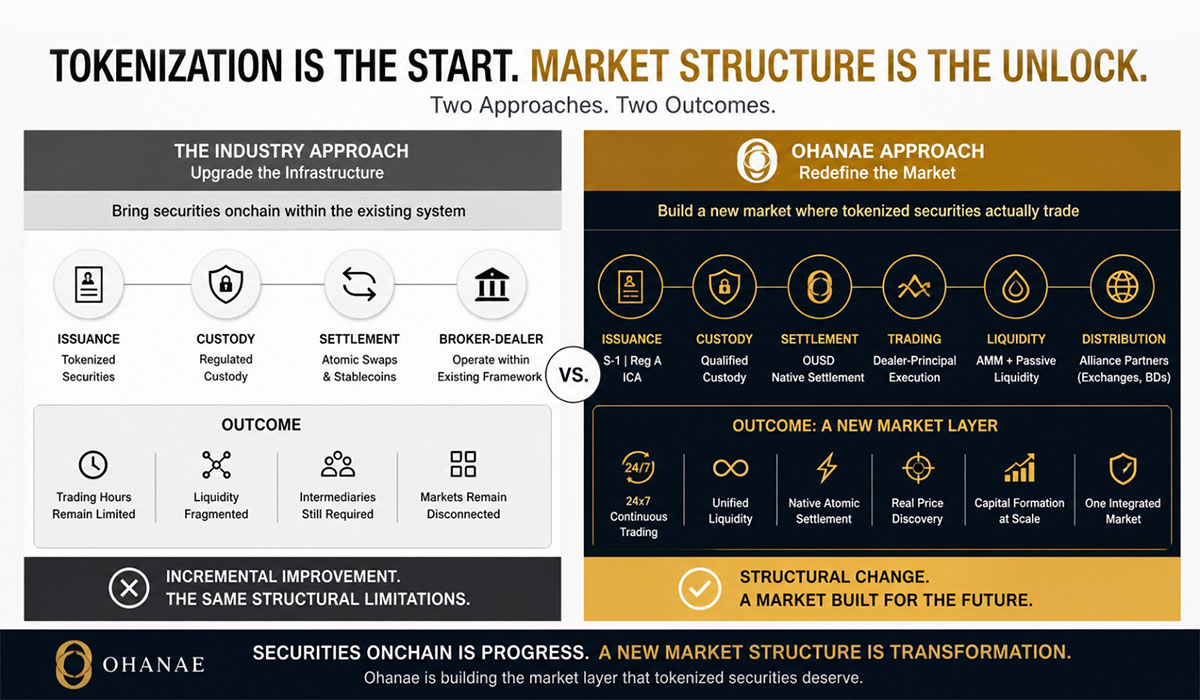

What the Industry Still Gets Wrong

Recent developments have reinforced a familiar narrative:

that tokenization—combined with custody and faster settlement—represents

the completion of market infrastructure.

It does not.

Bringing securities onchain, enabling atomic settlement, and operating within a regulated broker-dealer framework are meaningful advancements. They improve efficiency within the system.

But they do not change the system itself.

They remain anchored to the same structural limitations:

- Fragmented liquidity

- Intermediated market access

- Discontinuous trading environments

- Separation between issuance, trading, and settlement

These are not technical inefficiencies.

They are properties of the existing market structure.

Tokenization Without Market Structure Does Not Scale

Tokenization solves representation.

It does not solve:

- How liquidity is formed

- Where price discovery occurs

- How markets operate continuously

- How capital formation and secondary trading integrate into a single system

Without addressing these, tokenization becomes an overlay— a digital wrapper on top of a legacy framework.

The result is predictable:

incremental improvement without structural change.

The Misdefinition of “Full Stack”

The term “full stack” is increasingly used to describe platforms that combine:

- Issuance

- Custody

- Settlement

This is incomplete.

A market is not defined by its components.

A market is defined by its structure.

Without a native mechanism for:

- Liquidity formation

- Continuous trading

- Integrated distribution

- Unified execution

There is no market—only infrastructure.

Where Market Value Actually Accrues

In capital markets, value does not accrue at the point of issuance. Nor does it accrue at custody.

Value accrues at the market layer:

- Where buyers and sellers meet

- Where liquidity is formed

- Where price discovery occurs

- Where assets actually trade

This layer remains largely unaddressed.

The industry is beginning to recognize that tokenization alone is insufficient.

Liquidity, distribution, and market structure are now emerging as the defining challenge for digital securities markets.

Ohanae was built specifically to solve that layer.

A Clean-Slate Approach

Ohanae is built on a different premise:

That market structure—not tokenization—is the missing layer.

Not an upgrade to existing systems,

but a new market architecture designed for:

- Off-exchange operation outside Reg NMS

- Dealer-principal execution

- Continuous (24x7) trading

- Integrated issuance, trading, and settlement

- Native liquidity formation

In this model, tokenization is not the product.

It is the prerequisite.

Category of One

The industry is converging on a common direction:

bringing assets onchain.

Ohanae addresses what comes next:

Where those assets trade.

How liquidity is formed.

How markets operate when rebuilt from first principles.

Custody exists.

Tokenization is advancing.

Market infrastructure does not—yet.

That is the opportunity Ohanae was built to solve.