Abstract

Tokenization has been one of the most discussed innovations in financial markets over the past decade. Early implementations focused on replicating traditional securities through blockchain wrappers and structured vehicles. While these models demonstrated demand for digital assets, they largely operated around existing market infrastructure rather than within it.

A new phase is emerging.

Recent regulatory signals—including legislative developments such as the GENIUS Act, the CLARITY Act, and the SEC's Project Crypto initiative—suggest that policymakers are beginning to address the deeper structural question: how securities markets themselves may evolve in a blockchain-native environment.

The conversation is shifting from tokenizing assets to modernizing market infrastructure.

The First Wave of Tokenization: Engineering Around the System

The first generation of tokenized securities projects focused primarily on economic exposure.

Platforms created SPVs, wrapped securities, or synthetic instruments that allowed investors to gain exposure to traditional assets through blockchain tokens.

This approach made sense.

Traditional securities infrastructure—clearing, settlement, broker-dealer rules, and exchange regulations—was never designed for decentralized networks.

So innovators built workarounds.

These models helped prove market demand. But they also revealed their limitations.

Wrappers replicate securities exposure.

They do not transform how markets work.

A Shift in Regulatory Thinking

A significant signal recently emerged from the U.S. Securities and Exchange Commission during remarks related to Project Crypto.

Commission leadership stated:

"Specifically, I would like to consider how issuers that want to tokenize their securities could work with a transfer agent or other tokenization agent to tokenize their securities so that they can be traded onchain in AMMs or other trading systems, environments, or platforms that offer decentralized liquidity."

(Full remarks available here: https://www.sec.gov/newsroom/speeches-statements/atkins-peirce-021826-number-go-down-other-schadenfreude)

This statement matters because it acknowledges something the industry has been waiting for:

Regulators are beginning to consider how securities themselves could exist natively on-chain—rather than merely being wrapped representations.

That shift opens the door to deeper reforms across several areas:

- Transfer agent modernization

- Broker-dealer custody frameworks

- Capital formation pathways for digital securities

- On-chain secondary liquidity environments

In other words, regulators are starting to examine market architecture, not just asset classification.

Why the National Market System Still Matters

Traditional exchanges such as the New York Stock Exchange and Nasdaq remain foundational institutions.

They will continue to serve listed companies, public markets, and the core infrastructure of U.S. capital formation.

Tokenization does not replace these markets.

But it may expand the ecosystem around them.

In particular, a new category is beginning to attract attention: regulated markets for tokenized and exempt securities operating outside the National Market System (NMS).

These environments could support:

- early-stage capital formation

- alternative liquidity models

- blockchain-native settlement

- programmable ownership and compliance

This is not about replacing existing exchanges.

It is about completing the capital formation lifecycle.

From Workarounds to Clean-Slate Infrastructure

The most important evolution in the tokenization landscape may be philosophical.

The first phase focused on adapting blockchain to legacy systems.

The next phase focuses on designing market infrastructure specifically for tokenized securities.

That means starting with several core principles:

- cash settlement rather than margin leverage

- real-time ownership tracking

- blockchain-native custody and recordkeeping

- programmable compliance

- continuous liquidity rather than discrete trading sessions

These design choices fundamentally change how markets operate.

Settlement cycles shrink from days to seconds.

Ownership records become transparent and automated.

Liquidity models evolve beyond traditional order books.

A New Layer of Market Infrastructure

This is where a new category of regulated platforms is beginning to emerge.

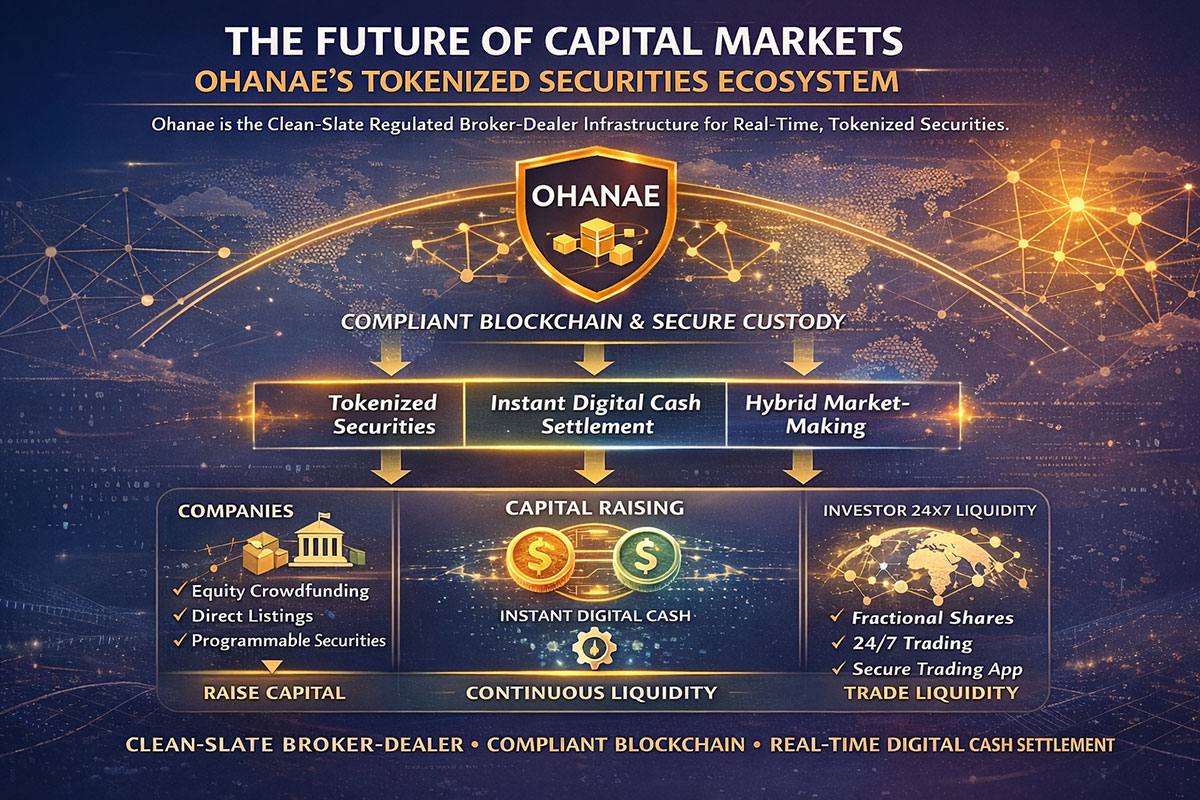

One example is Ohanae, a regulated broker-dealer infrastructure platform designed specifically for real-time tokenized securities markets.

NYSE. Nasdaq. Now, Ohanae.

Ohanae is building regulated infrastructure for tokenized securities that settle instantly with digital cash—bypassing traditional exchange settlement cycles.

The platform combines:

- broker-dealer custody

- compliant blockchain infrastructure

- automated ownership tracking

- continuous liquidity powered by automated market making

- 24x7 market access for investors

Its focus is not replacing public exchanges.

Instead, it aims to support tokenized and exempt issuers operating outside the National Market System, complementing existing market structure.

Why This Moment Matters

For years, tokenization lived in a regulatory gray zone.

Today, three forces are converging:

- Legislative clarity around digital assets

- Regulatory initiatives such as Project Crypto

- Institutional demand for blockchain-native capital markets

Together, they signal that tokenized securities may finally be moving from experimentation toward regulated market infrastructure.

If that transition occurs, the biggest opportunities will likely lie not in tokenizing individual assets—but in building the regulated systems where those assets trade.

The Road Ahead

Markets evolve slowly.

The New York Stock Exchange has operated for over two centuries. The Nasdaq revolutionized electronic trading decades ago.

Blockchain technology represents another potential step in that evolution.

But the real transformation will not come from wrappers or synthetic exposure.

It will come from new market infrastructure designed from the ground up for digital securities.

Confidence.

That’s the infrastructure the market has been waiting for.

Disclaimer

Ohanae Securities LLC is a subsidiary of Ohanae, Inc. and a member of the Financial Industry Regulatory Authority and Securities Investor Protection Corporation (FINRA/SIPC). Additional information about Ohanae Securities LLC is available on BrokerCheck.

Ohanae Securities LLC is currently in discussions with FINRA regarding the potential expansion of its business lines, which may include custody and related services for crypto asset securities. Any statements regarding the capabilities or services of Ohanae Securities LLC are subject to regulatory approval, and there can be no assurance that such approvals will be obtained.

Ohanae Securities LLC intends to operate in a manner that addresses the unique characteristics of crypto asset securities, including maintaining robust policies and procedures for custody, safeguarding of private keys, and evaluation of distributed ledger technology. The firm’s approach is designed to support crypto asset securities that may not efficiently operate within the traditional National Market System (NMS). Subject to applicable regulatory approvals, Ohanae Securities LLC may expand its activities to include additional services that may be conducted in a dealer-principal capacity, with the objective of protecting investors and maintaining market integrity.